Asian shares in a secular bull market

Key points

• Asian economies are undergoing a normal cyclical rebound on the back of a strong rebound in global trade, easy economic policies and strong domestic demand. Growth will likely remain robust going forward.

• While Asian shares have underperformed so far this year, partly on the back of worries about monetary tightening, the combination of reasonable valuations and stronger growth potential point to a resumption of relative outperformance over the years ahead.

Introduction

While Asia ex-Japan was hit hard by the global financial crisis (GFC), the region has bounced back just as dramatically, helped by stimulatory monetary and fiscal policies, a rebound in global trade and the absence of the secular constraints weighing on many advanced countries. The anticipation and then reality of this saw Asian shares dramatically outperform traditional global shares last year. However, so far this year Asian shares (flat) have underperformed traditional global shares (around +5%). Does this mean the outperformance by Asian shares has run its course? This note looks at both the economic and share market outlook for Asia ex-Japan.

Asian economic outlook

The rebound in Asian economies (ex-Japan) is evident in a range of indicators, most notably industrial production and exports. For example, annual growth in exports has gone from an annual decline of more than 20% at the start of last year to over 30% annual growth now. Consumer spending and investment have also picked up.

.jpg)

The economic recovery in Asia is clearly evident in gross domestic product (GDP) growth, with latest annual GDP growth running at 11.9% in China, 13.1% in Singapore, 9.2% in Taiwan, 7.8% in Korea and 6% in India. Our leading indicator for growth in the region, based on a composite of indicators which lead economic activity, points to further acceleration ahead.

.jpg)

Basically, Asia has undergone a pretty normal cyclical downturn from which it is now rebounding. It is not lumbered with the combination of secular constraints in the form of high public and private debt levels, weakened financial systems and poor demographics that are likely to constrain growth in Europe, Japan and the US. Rather it is likely to continue to benefit from strong productivity growth, a shift to greater reliance on domestic consumption, ongoing industrialisation and urbanisation, and a continued catch-up to advanced country living standards.

One concern in Asia is that inflation has started to return, highlighting that monetary conditions will need to be returned to normal sooner rather than later.

.jpg)

Some countries have already commenced this process, including China, India, Malaysia and Singapore. However, there is likely further to go and the process of monetary tightening going forward is likely to involve allowing exchange rate appreciation.

Overall, we see growth settling down to a medium term pace of around 6% across the Asian region, ranging from around 9% in China to 5% in Asean countries. This would translate to nominal growth of around 8% per annum (p.a.). The risk is that this is too conservative.

Secular bull market in Asian shares has further to go

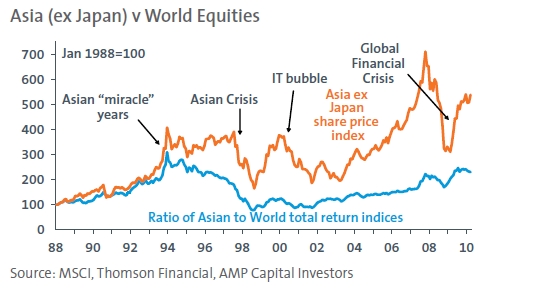

While US and European shares have been in a secular bear market over the last decade and Japan since 1989, Asian shares have been in a secular bull market since 2001; as seen in a pattern of rising highs and rising lows in the MSCI Asia ex Japan share index. This is evident in Asian shares’ relative outperformance versus global shares over the last decade, which remained intact despite the slump in Asian shares during the GFC. The next chart shows the performance of Asian equities in absolute terms (top line) and relative to global equities as measured by MSCI indices (bottom line). When the relative return line is rising, Asian shares are outperforming global shares and vice versa for falls.

It is worth noting the ratio in the previous chart (i.e. the blue line) remains below 1990’s peak levels, suggesting Asian outperformance may still have a long way to go.

Reasons to be overweight Asian shares strategically

So far this year Asian shares have underperformed global shares, reflecting a pause after last year’s strong outperformance and in response to the move to monetary tightening in Asia ahead of the US. However, this is likely to be no more than a temporary setback. There are still numerous reasons to believe Asian shares will outperform global shares over the next five to 10 years.

First, Asian countries do not suffer from high levels of consumer and public sector debt that are likely to constrain growth in the US, Europe and Japan in the years ahead. If anything, high household savings rates and low consumer debt mean there is plenty of potential to boost consumer spending going forward.

Second, the financial system (and hence credit growth) in Asia is unlikely to be constrained as it likely will be in the US and Europe by increased financial regulation in the wake of the GFC.

Third, Asian countries are highly dynamic and clearly focused on achieving western per capita income levels. However, they still have a lot of catching up to do which means plenty of potential going forward.

Fourth, Asia generally benefits from more favourable demographics. Asia, along with most other emerging markets (excepting Eastern Europe), is projected to have faster population growth and a lower dependency ratio (i.e. the ratio of children and retirees to working age people) than in developed countries. This contributes to a faster growth rate in the labour force and hence faster potential economic growth overall. China is an exception, but it still has a large underutilised rural workforce it can draw on.

All of these points so far suggest strong economic growth relative to growth in the US, Europe and Japan.

Finally, Asian equities are trading on a slight discount to global shares. This is evident in the next chart, which compares the ratio of share prices to consensus year-ahead earnings expectations for Asia and global shares. Note the huge post-Asian crisis discounts are no longer required given Asia’s stronger fundamentals.

.jpg)

Asia to outperform over the next few years

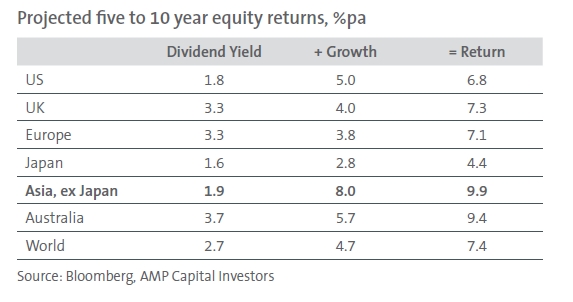

The table below provides a rough guide as to potential share market returns over the next five to 10 years. They are based on current starting point dividend yields and assume share prices rise with nominal economic growth, so that the total return for an investor is the dividend yield plus nominal GDP growth. On the basis of our arguably too conservative nominal growth assumption of 8% p.a., Asian shares offer a return potential well ahead of other major regions. While actual returns are likely to be wildly different than those shown in the table, the stronger growth potential in Asia supports the case for several years of outperformance from Asian shares.

Conclusion

Asian shares are likely to be relative outperformers over the next few years, helped by reasonable valuations and relatively strong growth prospects.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital Investors