Falling commodity prices - more good news than bad

14 August 2008

Key points

- After a longer than normal delay, commodity prices have entered a significant correction on the back of slumping global growth and a stronger US dollar (US$).

- This is good news for the global growth outlook and for shares generally as it takes pressure off inflation and allows for lower interest rates. However, it is bad news for resource shares and the Australian dollar (A$).

- While the correction in commodity prices has further to go, their long-term trend is likely to remain up.

Introduction

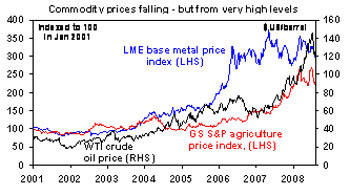

Commodity prices have fallen sharply. From recent highs, oil, gold and copper prices have fallen around 20% and wheat and corn prices are down around 30%. Of course this has occurred from very high levels. See chart below.

What is driving the slump in commodity prices? What are the implications? Is this the end of the commodity bull market or just a correction?

Commodity prices and the global growth cycle

In a normal global economic downturn, commodity prices fall in response to slowing economic activity. This takes pressure off costs and inflation, allowing interest rates to fall which sets the scene for an economic rebound. This time around has been a bit different. Until a month or so ago, commodity prices remained very strong. They were being propelled by: strong growth in the emerging world (notably China); investor demand for commodities as a hedge against a falling US$; and speculative demand made possible by the growth of commodity funds and investor scepticism with financial assets.

The problem was that the surge in commodity prices, notably for oil, was not only cutting into profit margins and consumer spending power but that it was directly adding to global inflation. Consequently, this was keeping global central banks far more hawkish than they should have been. Thus, while the credit crunch meant interest rates should have been falling, in most countries they were actually being left on hold (e.g. US and UK) or increased (e.g. Europe and Australia). The end result has been more global economic pain than would normally be the case.

Back to normal

The past month has started to see commodity prices return to something like their normal relationship with the global growth cycle, with sharp falls now becoming evident. There are several reasons for this.

- Recent data has shown that Japan and Europe are flagging just as badly as the US (if not worse). In fact, the recent flow of economic indicators suggests that both regions may now be in recession. This is bad news for the emerging world (including China) because they will find it harder to divert their exports away from the already weak US.

- It has become increasingly clear that China, India and other emerging countries are also slowing. Chinese economic growth looks like being 9% to 10% this year compared to last year’s near 12%. As a result, Chinese authorities are now starting to back pedal on some of last year’s tightening. Indian growth is likely to slow back to 7% from 9% last year, with aggressive monetary tightening starting to bite. Growth in Brazil is also likely to slow on rising interest rates.

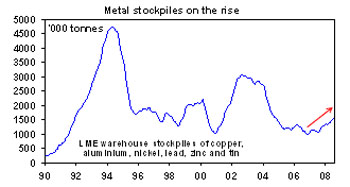

- The slump in share markets as oil went through US$120 a barrel in May and increasing evidence of falling oil demand indicated that the surge in the oil price was starting to “choke off” growth and hence oil demand. Rising base metal inventories are also starting to become evident. See the chart below.

- The realisation that growth outside the US is now slowing faster than that in the US has seen the US$ break higher. This, in turn, has suddenly removed investor demand for commodities (such as oil and gold) as a safe haven against a falling US$.

The combination of all of these developments has seen commodity speculators squeezed. The favourite trade recently was long oil/short banks, but in the last few weeks it has suddenly reversed. This has forced investors to close their positions, thus increasing the severity of the moves.

A pause, not the end, in the commodity super cycle

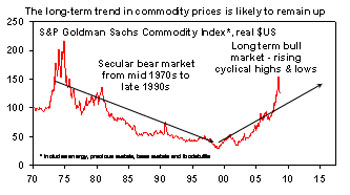

China may be slowing, but is not about to collapse and the long term demand potential in emerging countries is huge. China’s copper usage per person is less than half US levels and its oil usage per person is around 10% that of developed countries. Rising income levels and the increased use of agricultural products for fuel will also see ongoing upwards pressure on agricultural demand. Just as we have seen in the last six years, supply will struggle to keep up with commodity demand over the long term. As such, the long term trend in commodity prices is likely to remain up. See the chart below.

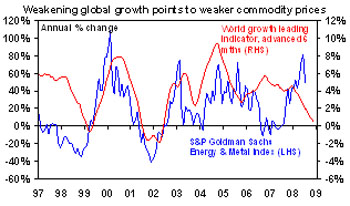

In this context, the recent pull back in commodity prices should be seen as a correction, but it likely has further to go. Commodity prices remain well above their rising trend (as evident in the previous chart) and speculative positioning and sentiment regarding commodities is yet to fall back to levels associated with a durable rebound. The economic news over the next six months is likely to get worse before it gets better. The next chart shows the relationship between a leading indicator of world growth (based on the OECD’s leading indicators for OECD countries plus Brazil, Russia, India and China) and commodity prices. Normally, there is a close relationship but it broke down last year and into mid this year as the leading indicator fell yet commodity prices surged. However, a more normal relationship seems to be getting re-established. As can be seen below, the leading indicator suggests more weakness in commodity prices ahead.

Against this backdrop, speculative positions in commodities are likely to be wound back further (particularly as the US$ now seems to have regained a firmer footing). In the very short term, commodities have become oversold and due for a bounce. However, the trend over the next six months or so is likely to remain down.

Implications – the good and the bad

The cyclical downturn in commodity prices that is now underway has a number of implications:

- The correction in commodity prices is good news for the global economic outlook and share markets generally. Softer commodity prices will remove much of the pressure on inflation and allow global central banks to lower interest rates and provide greater flexibility to deal with the ongoing credit crunch. We expect lower interest rates in Europe, the UK, Japan and Australia over the next six months. Lower commodity prices will most likely: help reduce corporate cost pressures; provide increased consumer spending power; make it easier for a healing of the global economy; and be generally positive for global shares.

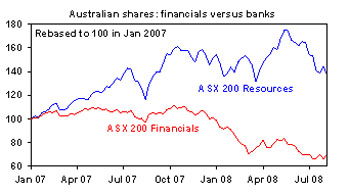

- Falling commodity prices, while generally being good for shares, are actually bad news for resources shares. As such, there is potential for a further reversal of their relative outperformance versus financial shares over the last year. See the chart below in relation to Australian resources and financial shares.

- Given the relative importance of resources in the Australian share market, it is likely to mean that Australian shares may underperform global share markets for a while yet, as the commodity correction continues to run its course. Asian shares are likely to be key beneficiaries of the correction in commodity prices given Asia’s high reliance on commodity imports.

- The commodity price downswing means the A$ has entered a cyclical correction greater than any of the pullbacks seen in recent years. While the A$ is oversold (having fallen 13% in four weeks) and may therefore have a short-term bounce, more downside is likely in the months ahead, possibly to US$0.80. Parity against the US$ has been postponed, probably till late 2009 after the commodity cycle turns up again.

- A downturn in traded commodity prices will also dampen the terms of trade boost for the Australian economy, adding to the case for Reserve Bank of Australia (RBA) interest rate cuts.

Conclusion

Commodity prices have entered a cyclical correction which looks like running a bit further. While this is bad news for resources shares, the relative performance of Australian shares and the A$, it’s necessary to clear the way for lower interest rates to combat the credit crunch. Overall, it’s more good news than bad. Broadly, we think that the commodity super cycle remains alive and well, but a sustained resumption of the uptrend in commodity prices probably won’t get underway until some time next year.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital Investors

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591) (AFSL 232497) makes no representation or warranty as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.