Prospects for a "happy" new year

Looking forward to a new calendar year, there is perhaps more reason to be pessimistic about Australia’s economic prospects than has been the case for some time. Interest rates and inflation have adjusted upwards, the drought has taken grip of our rural communities and there has been virtually no improvement in productivity.

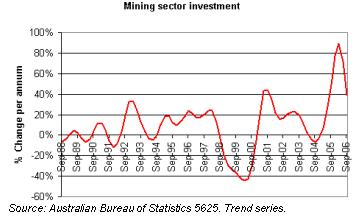

Earlier this decade, the housing and household consumption boom provided a strong catalyst for economic growth. Just as this boom faded away in most regions, the surge in commodity prices and mining industry investment (eg spending on machinery and opening new mines) provided a replacement stimulus to the economy. However, with commodity prices and mining industry investment looking to have peaked (see chart below), there is no obvious new “driver” of economic growth in the lead up to 2007.

The recent economic growth performance

In discussing the Government’s forthcoming changes to its economic and budget projections, Treasurer Mr Costello has hinted of tougher times ahead. The Treasurer suggested that “a couple of things have changed very significantly since we brought down the Budget.” One of these changes is that the rate of economic growth has not picked up as expected.

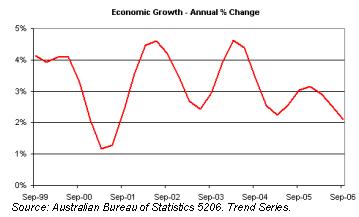

At the time of handing down its budget in May, the Government was anticipating an economic growth rate of 3.25% for the 2006/07 financial year. This is more than a full percentage point higher than the rate of growth of 2.2% in the year to September 2006. With the latest quarterly growth rate being just 0.3%, it would require a significant pick up in activity for the Government’s budget time estimate to be met.

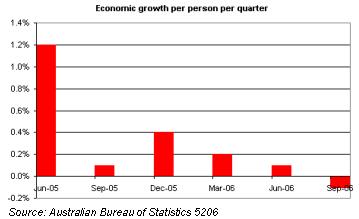

The lack of momentum in economic growth in Australia currently is highlighted by the fact that the economy failed to expand by more than the rate of population growth in the 3 months to September this year. As shown on the chart below, the negative movement in growth (adjusted for population) follows a string of very low quarterly growth rates over the past year.

Does growth matter?

The fact that the Australian economy failed to produce more material output for each of its members over the past quarter is generally considered to be bad news. Economic growth is undoubtedly a key policy objective of the Government and is the primary mechanism by which the living standard of Australians is able to improve.

However, with the environmental implications of economic growth being increasingly understood and witnessed in the community, many have cause to questions the merits of continued economic expansion. There is also mixed empirical evidence as to the extent to which economic growth leads to greater individual “happiness”. The so-called “Easterlin Paradox” suggests that happiness does not increase as the level of Gross Domestic Product (GDP or material output) increases.

Leaving this philosophical question around the relationship between happiness and economic growth to one side, there are very real consequences that may flow from a continuation of very modest economic growth into 2007.

First and foremost, if the downward trend evident in Australia’s economic growth rate (see chart above) was to continue, the demand for workers would start to contract. The economy could then enter a “vicious circle” whereby rising unemployment leads to falling household expenditure, which in turn leads to additional increases in unemployment. This is a pattern of activity that the Australian economy has luckily not seen for some time.

For investors, a period of significantly weaker economic growth would impact on equity market returns. Much of the ability of the corporate sector to improve earnings comes about through the expansion in demand facilitated by a growing economy. As evidenced by the Japanese economy over much of the past decade, the absence of economic growth makes it very difficult for company profits, and therefore sharemarket values, to increase.

In theory, a weaker rate of economic growth should allow interest rates to fall (as there is less demand pressure on inflation). However, this assumes that the value of the currency remains stable. For an economy with a large foreign debt, such as Australia, a period of weak economic growth may lead to a rise in debt to income ratios and spark concerns over debt servicing. This concern may then put downward pressure on the value of the currency, thereby increasing import prices, inflation and ultimately interest rates.

It’s not all doom and gloom

Whilst the recent trend in economic growth has been clearly downwards, and there is little prospect that 2007 will herald a return to giddy heights, the Australian economy does have a few factors working in its favour.

The current low rate of unemployment should underpin reasonable household sector spending over the course of next year. With retail spending by households being the largest source of demand in the economy, we should be able avoid a downward growth spiral so long as this retail spending remains at least moderate.

Secondly, the Federal Government has placed itself in an extremely strong financial position, with an absence of debt. It therefore has a large capacity to increase spending should the economy start to fail. With various pieces of infrastructure in need of additional financial support, the economic case for increased spending may be relatively easy to create.

Thirdly, with international conditions remaining favourable, Australia is still likely to reap benefit from the mining boom and the considerable investment that has gone into generating additional capacity in this sector. This should see a continuation in the growth of non-rural exports, providing additional stimulus to growth and helping to stabilise the foreign debt position.

Summary

1. Economic growth has weakened in the lead up to the new year, with the latest quarterly number showing a contraction in per person economic output.

2. Notwithstanding ongoing philosophical debates about the importance of economic growth, a prolonged period of growth weakness would have detrimental implications for employment levels and investment returns.

3. Although there is no catalyst currently identifiable to substantially boost economic growth in 2007, the fundamentals of the Australian economy appear sufficiently sound to ensure the economy will avoid recession like conditions for the next year at least.

Brad Matthews, Hillross Economist