Oil and shares – this year’s Factor X

Key points

· The oil price is now critical to the outlook for shares.

· While the long-term trend in the oil price will likely remain up, current prices are not justified by oil supply and demand and are likely to fall back (probably to around US$100 a barrel) in the next six months.

· If the oil price continues to surge, shares will remain under pressure. Iran and hurricanes are the wildcards.

Oil is the key

The big slump in shares from their highs in October/November last year to their lows in March this year was driven primarily by the credit crunch. However, the continued surge in the oil price has played a major role in the slump in shares since mid-May which has now taken them below their March lows. The dramatic rise in the oil price is now a major threat to economic growth. It has also exacerbated the credit crunch by pushing up inflation and, hence, market interest rates. This has offset the US Federal Reserve’s interest rate cuts, made global central banks more hawkish and increased the risk of debt defaults. While US Treasury moves to support Fannie Mae and Freddie Mac should help provide a bounce for shares, if the oil price doesn’t turn around soon, a global recession will become a certainty and shares will fall further. But if the oil price does manage to stabilise and start heading back to earth, shares will likely receive a huge boost.

Fundamentals support a rising trend in the oil price

For many years, our view has been that the rise in the oil price has been justified by fundamental supply and demand considerations. As countries like China and India industrialise (and use more energy in the process), the supply of oil is struggling to keep up. Per capita oil usage in China and India has been rapidly rising. Even though this has been occurring from a low base, the huge population of both countries has meant a massive rise in oil demand. China now accounts for around 70% of the annual increase in global oil demand, and this is set to continue. For example, if per capita oil consumption in China and India were to rise to just half of Australian levels, it would imply an extra 40 million barrels per day in global oil demand (which is currently 86 million barrels a day). At the same time, the sources of cheap easily extractable oil are drying up. As a result, the long-term trend in the oil price is being driven by demand and supply factors and will remain up.

Has it become a bubble in the short term?

Over the last six to twelve months, the rise in the oil price has become exponential, even though the supply and demand situation has not really changed that much. This suggests it may be starting to run ahead of fundamentals. Speculative manias tend to have several key elements:

· Easy money and low interest rates;

· A fundamental dislocation which underpins initial price gains and provides enthusiasm for the eventual mania;

· A means to allow mass speculation; and

· The extrapolation of past price gains into the future

Many of these are now arguably present in the case of oil.

· The cut in US interest rates has provided the easy money backdrop and the associated fall in the US dollar has increased demand for commodities as a hedge against dollar weakness. Falling share markets have also encouraged investment flows into commodities;

· The China story and all the talk about ‘peak oil’ has helped provide a fundamental justification;

· The advent of commodity funds investing into futures has provided a means to easily invest in commodities. These have up to 74% benchmark weights in energy; &

· Analysts have been falling over themselves trying to come up with even higher predictions for the oil price. Expectations of US$150 to US$200 are now common.

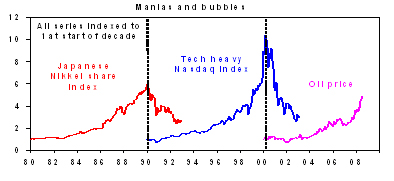

The surge in the oil price is certainly starting to look like past bubbles, such as the bubble in Japanese shares in the late 1980s and the technology bubble in the late 1990s. Specifically, prices rise steadily for many years, justified by fundamentals, only to then start rising exponentially.

Source: Thomson Financial, AMP Capital Investors

Of course, the argument that the surge in the oil price has become speculative has been subject to much debate. Some have argued that it is hard to find definitive proof of speculative involvement. Measures of speculative positioning in oil and sentiment are mixed. But then again, it is always hard to prove that price surges are due to speculative bubbles. It has also been argued that there cannot really be a speculative mania in oil because if there were, then demand would dry up, production would surge and stockpiles would go through the roof burning the speculators. This has not happened. However, against this it may be the case that demand is just responding with a long lag. Supply growth may be struggling to keep up with demand but the situation has not changed so much over the last year to justify a doubling in the oil price. There is also an argument that futures pricing plays a much bigger role in the setting of spot oil prices than in the case of other commodities, because Saudi Arabia actually uses oil futures prices to set sale contract prices.

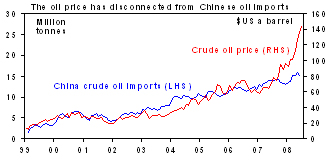

The chart below also suggests that the exponential rise in oil prices this year has disconnected from Chinese oil demand. Over the last decade, China’s oil imports have steadily increased. Even though this remains the case, the crude oil price has gone exponential over the last year.

Source: Bloomberg, AMP Capital Investors

Signs of an oil price correction on the way

Bubble or not, for the following reasons, it appears increasingly likely that the oil price has gotten ahead of itself in the short term and the fundamental backdrop is starting to move against oil prices:

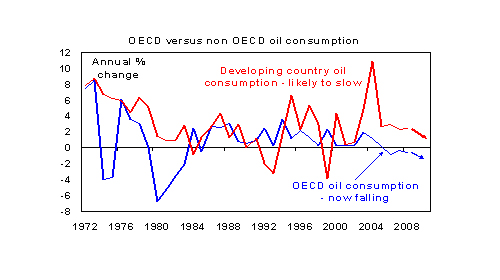

· For the rich world it has become increasingly obvious that the ‘choke point’ has been reached. This particularly relates to the speed with which the oil price rises. The oil price rose dramatically over the 1998 to 2007 period but the ‘three steps forward one step back’ process gave businesses and consumers time to get used to it. The doubling over the last year is a lot different and has come at a time when key economies are already struggling on the back of the credit crunch. This is showing up in falling oil demand in these countries.

Source: AMP Capital Investors

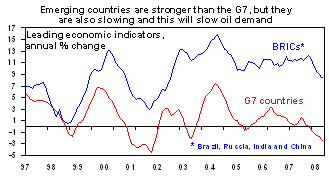

There are now numerous indications that the same will occur in the emerging world. Slower growth in rich countries is leading to a slowdown in emerging world exports. This is clearly evident in China where export growth has slowed dramatically. Monetary tightening in response to rising inflation will lead to slower demand growth in these countries going forward, particularly in Asia where inflation has become more of a problem. As a result, the OECD’s leading indicator for developing countries has slowed significantly. Share market collapses in these countries are also warning of much slower growth ahead. For example, Chinese and Indian shares have fallen 56% and 38%, respectively. This, along with rising fuel prices in such countries, is likely to start slowing emerging world fuel demand over the year ahead.

Source: Bloomberg, AMP Capital Investors

A risk premium of US$10 to US$15 a barrel for the threat of conflict between Israel and Iran has been priced into oil. If Israel has a military fight with Iran, the sky is the limit for the oil price in the short term. Iran produces 4.3 million barrels a day, of which it exports 2.5. If this is taken out it will use up all of OPEC’s spare capacity. How this unfolds is anyone’s guess. However, assuming commonsense prevails, the risk premium should fade over the next few months. The other wildcard is the US hurricane season, which could also adversely impact short-term oil supply.

With speculators now playing a big role in the oil price, the very short-term outlook is hard to predict. The oil price could easily spike higher. But the bottom line is that barring a major disruption to oil supplies, the oil price is likely to fall sharply at some point in the next six months, probably to around US$100 a barrel, in response to weaker oil demand.

Oil is the factor ‘X’ for shares

It appears increasingly likely that the surge in oil prices is this year’s factor ‘X’ for the global economy and shares. Where the oil price goes from here is critical. We remain of the view that while shares are due for a short-term bounce (and US Government support for Fannie Mae and Freddie Mac may help provide this) the next few months are likely to be rough. We anticipate that shares will rally hard in the fourth quarter on the back of very attractive valuations once the news flow starts to improve. Things to look for to confirm this is on track include:

· A sharp and sustained fall in the oil price;

· A fall in inflation worries as represented in bond yields;

· A relaxation in central bank hawkishness;

· A slowing in US house price falls; and

· A sustained improvement in credit markets.

Dr Shane Oliver

Chief Economist and Head of Investment Strategy, AMP Capital Investors