Rising Australian interest rates - how far, how fast?

Key points

- More increases in Australian interest rates are likely in the year ahead as the Reserve Bank of Australia (RBA) seeks to move rates towards normal levels. The normal level is now judged to be around 5%.

- The process of tightening is likely to remain gradual due to falling underlying inflation and lingering uncertainties about growth. The cash rate is unlikely to reach 5.00% until around the end of 2010.

- Rising interest rates won’t be a major problem for shares until rates reach onerous levels. This is unlikely until 2011 or 2012. The key rate to watch is the US Federal Funds rate where rate hikes are still some time off.

A rising interest rate differential in Australia’s favour will heighten upward pressure on the Australian dollar (A$), with another go at parity likely in the next 6 months.

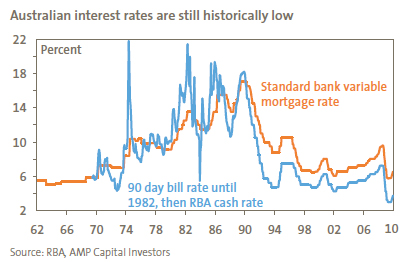

Australian interest rates have further to rise

The RBA has again increased the cash rate by another 0.25% taking it to 3.75%. While much will no doubt be made of the fact the RBA hasn’t increased rates three months in a row since the 1980s, it should be noted that 3.75% is still very low for the cash rate from a historical perspective. Refer to the chart below.

Bank mortgage rates also remain historically low. Assuming the average bank’s standard variable mortgage rate moves up by the 0.25% hike in the cash rate, this would take the rate to around 6.50%. Apart from in recent months, the last time it was lower than this was for a brief period just after the 9/11 terrorist attacks, and prior to that was in the early 1970s.

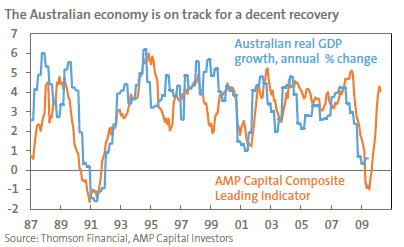

While the latest statement from the RBA is non-committal regarding interest rates going forward, the RBA’s generally upbeat tone suggests that more rate hikes are likely if the economy continues to recover as expected. This is consistent with our own composite leading economic indicator which is pointing to 4% economic growth over the year ahead.

While there was a case to hold fire this month, in terms of the big picture there is no need for interest rates to remain at historically low levels provided economic growth continues to head back above trend.

The ‘new normal’ for the cash rate

The normal level for the cash rate is basically the level below which monetary policy stimulates the economy, but above which it acts to slow the economy. So, the big question is what is the ‘normal’ level for the cash rate? This is important because it may provide a rough guide as to where the RBA is likely to take the cash rate in the next year or so.

In the past, the normal rate was thought to be around 5.50% to 6.00%. In theory, the normal level of interest rates should be around a country’s potential nominal gross domestic product (GDP) growth rate. For instance, if Australia’s long-term inflation rate is going to be at the mid point of the inflation target (i.e. 2.50%) and potential real GDP growth is around 3.00%, then this would imply a normal rate of 5.50%. Surprisingly, the average level for the cash rate over the period since inflation targeting began is 5.50%.

However, several considerations suggest the normal level of interest rates may have changed. Two factors are likely to be pushing it up. These are stronger population growth, on the back of higher immigration levels, and the boost to national income and mining investment from the commodity boom, which we suspect has much further to go. Against this though, several other factors suggest the normal interest rate may have declined:

- Bank lending rates are running at higher levels relative to the cash rate than has been the case in the recent past. For example, over the 10 years to December 2007, the gap between the standard variable mortgage rate and the cash rate was 1.8 percentage points. It is now 2.8 percentage points. Assuming the gap remains this high, the RBA won’t need to increase the cash rate as much to attain a given level for private sector borrowing rates. The 1.0 percentage point difference in the spread between the mortgage rate and the cash rate would suggest that the normal cash rate is now 1.0 percentage point lower than it was two years ago.

- The level of household debt to income has increased in recent years. The result is that households are likely to be more sensitive to interest rate increases than in the past. In other words, the RBA won’t have to increase the cash rate as much to achieve a slowing in the economy.

- The A$ is running well above the average level that prevailed since the float of around US$0.70, and this will be having a constraining impact on the economy.

Weighing up these conflicting forces suggest to us that the normal cash rate has fallen to around 5%

With growth improving (but underling inflation falling due to excess capacity globally), the strong A$ bearing down on import prices and uncertainty remaining regarding the strength of the global recovery, our assessment is that the RBA can continue taking a very gradual approach in raising the cash rate. In fact, having increased the cash rate three months in a row, there is a case for the RBA to see what the impact has been before moving again. This suggests that the next hike may not be until March 2010.

Our view remains that the 5.00% level for the cash rate in Australia won’t be reached until the end of 2010 and, in the absence of inflationary pressures, monetary policy won’t move into tight territory until 2011 or 2012.

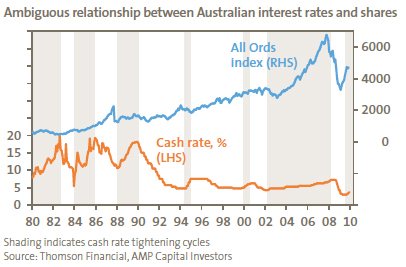

Interest rates and shares

There is an ambiguous relationship between rising interest rates and the share market. While higher rates places pressure on share market valuations by making shares appear less attractive, early in the economic recovery cycle this impact is offset by improving earnings growth. The chart below shows the official cash rate and share prices in Australia since 1980, with cash rate tightening cycles shaded. Sometimes rising interest rates have been bad for shares, as in 1994 for example, but other times this has not been the case. For example, between 2003 and 2007 shares went up as interest rates rose.

Several considerations are worth noting.

Firstly, rising interest rates from a low base are not normally initially bad for shares, as they go hand-in-hand with improving economic conditions (just like falling interest rates in a recession are not initially good for shares, as occurred last year). For example, this was evident during the initial stages of monetary tightening in the late 1970s and early 1980s, the 1984 tightening, through 1988 and much of the 2002 to 2008 tightening.

Secondly, rising interest rates are only a major problem for shares when rates reach onerous levels (i.e. above normal), contributing to an economic downturn, e.g., in 1981 to early 1982, late 1989, and in late 2007 to early 2008. They are also a problem when rate hikes are aggressive, as was the case in 1994 when the cash rate was increased from 4.75% to 7.50% in just four months.

Finally, given the high short-term correlation between Australian shares and US shares, what the US Federal Reserve does is arguably far more important than local interest rates.

Thus, in terms of the current situation, the rise in Australian interest rates from 3% to 3.75% is not likely to derail the cyclical bull market in shares as:

- Rising interest rates reflect economic recovery rather than a sign of an eventual growth downturn, so the improving profit outlook will provide an offset;

- Interest rates are still at generational lows, and with inflationary pressures so subdued it will be some time before interest rates reach onerous levels. In fact, this is not expected until 2011 or 2012 when the cash rate will rise above the ‘normal’ level of 5%; and

- US rate hikes are unlikely until mid 2010 at the earliest.

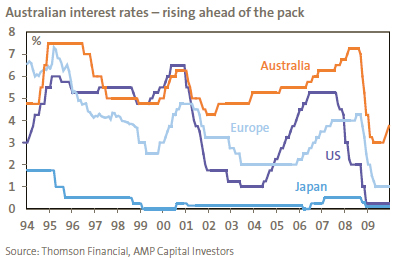

Interest rates and the A$

The A$ is already up sharply from its US$0.60 low last year. With the interest rate differential between Australia and other major countries getting wider, and commodity prices likely to see more upside, the upward pressure on the A$ is likely to intensify.

We remain of the view that the A$ will breach parity against the US dollar sometime in the next 6 months.

Concluding comments

Interest rate hikes next year in Australia are likely to be more gradual, taking us up to around 5.00% by year end. Only when rates move noticeably beyond this and US interest rates rise above normal will interest rates be at levels judged restrictive enough to hurt the economic outlook, and hence shares.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital Investors